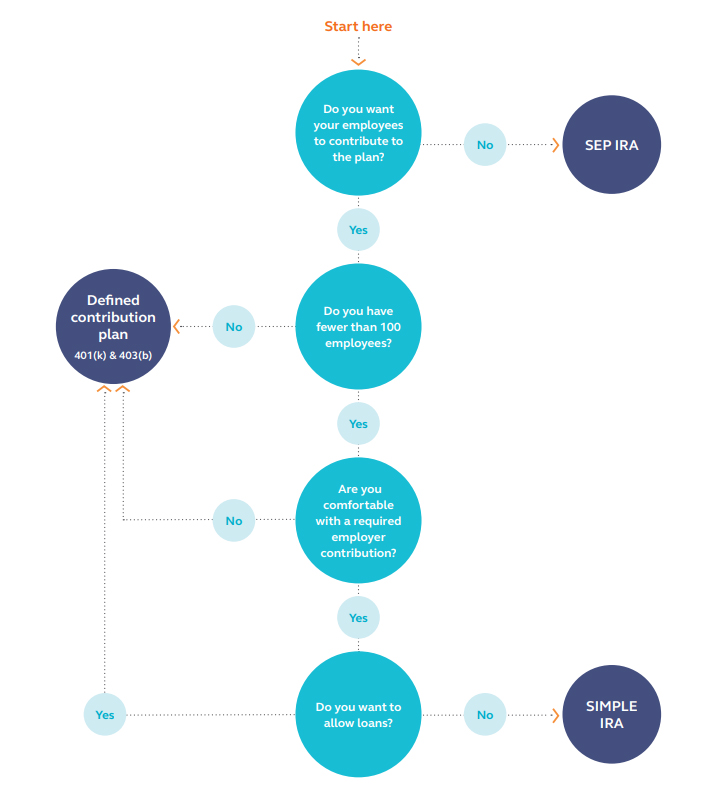

MAJOR TYPES OF RETIREMENT PLANS Various types of retirement plans are offered to small company owners. The significant ones consist of the following (see the chart, "Comparison of Retirement Plans for Small Companies," for more information on the four most typical types of plans): Simplified staff member pension (SEP) plans SEPs can be used by services with any variety of employees.

The main advantage of SEP plans is how simple they are to administer. After adoption, no yearly internal revenue service kinds normally need to be filed for a SEP, and administrative costs are very little. There are 3 actions to establishing a SEP. The company should (1) perform a written arrangement to supply benefits to all eligible employees; (2) give workers specific information about the arrangement; and (3) establish an IRA account for each worker.

However, not all employers can use Form 5305-SEP, and rather some need to use a model file. Nevertheless, SEPs do not permit staff members to postpone income, and workers are constantly 100% vested in company contributions to their SEPs. Therefore, they might not be the very best choice for business in industries with high employee turnover or that wish to use a retirement strategy to help maintain workers.

Due to the fact that of this requirement, a smaller company with a self-employed owner might lack sufficient capital to support such a plan if the owner wishes to make a big contribution to his/her SEP. Cost savings reward match prepare for employees (EASY) individual retirement account plans SIMPLE Individual retirement accounts are generally offered to companies with 100 or less employees who got $5,000 or more in settlement in the preceding year.

As the name suggests, easy IRAs are simple to carry out and administer. To execute this strategy the employer can use Type 5304-SIMPLE, Cost Savings Reward Match Prepare For Workers of Small Companies (SIMPLE) Not for Use With a Designated Banks, or Type 5305-SIMPLE, Cost Savings Reward Match Plan for Workers of Little Companies (SIMPLE) for Usage With a Designated Banks.

A little employer may wish to execute a BASIC IRA strategy because it permits staff members to delay income by making salary reduction contributions (subject to annual limitations) to their SIMPLE Individual retirement accounts. Another possible benefit to an employer of an EASY IRA strategy over a SEP is that it normally requires a smaller sized contribution on the company's part.